Editorial – by the Publisher

Georgia’s SB 424 Is Goldbuggery, Not Governance

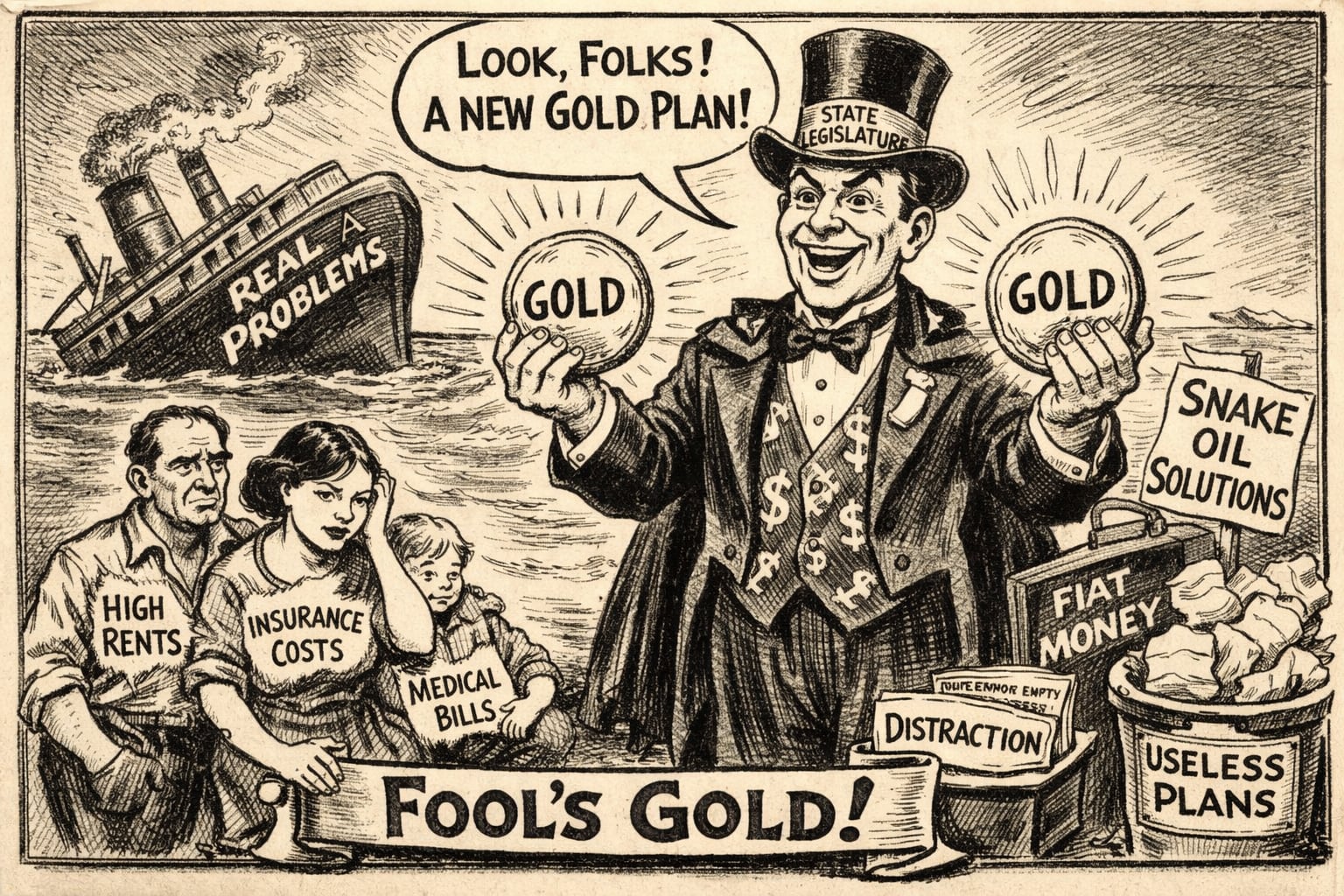

Augusta, GA – While Georgia families wrestle with high rents, rising insurance premiums, healthcare bills, and lingering inflation anxiety, lawmakers under the Gold Dome are advancing Senate Bill 424 — the “Transactional Gold and Silver Act.”

Sponsored by State Sen. Marty Harbin, a Republican from Tyrone, and backed by bipartisan support including Sen. Sonya Halpern, a Democrat from Atlanta, SB 424 would allow Georgians to purchase fractional amounts of gold and silver bullion and use those holdings through an electronic payment system — essentially a debit-style account backed by precious metals. The proposal envisions a state-supervised bullion depository structure and would exempt gold and silver transactions from Georgia capital gains taxation. According to recent reporting, the system could rely on a private processor such as UK-based fintech firm Glint Pay to handle logistics.

Supporters describe the bill as a hedge against inflation and a tool for “economic freedom.” They point to gold’s long-term record as a store of value and argue that fiat currency — untethered from the gold standard since the early 1970s — has steadily eroded purchasing power.

It is an appealing narrative.

It is also economically thin.

Fiat Money Is Not a Fragile Illusion

Modern fiat currency does not derive its value from metal backing. It derives its value from institutional design.

The U.S. dollar is sustained by several structural pillars. Federal taxes must be paid in dollars, creating constant demand. Wages, contracts, mortgages, insurance policies, and state budgets are denominated in dollars. U.S. Treasury markets provide deep liquidity and serve as global reserve assets. The Federal Reserve controls national monetary policy, interest rates, and system-wide liquidity.

None of this changes because Georgia authorizes gold-backed debit cards.

As long as federal income and payroll taxes must be paid in dollars — and they must — demand for dollars remains compulsory. As long as contracts and prices are written in dollars — and they are — the dollar remains the unit of account.

SB 424 does not challenge federal monetary authority. It operates entirely within it.

Georgians Already Can Buy Gold

Another crucial point often left unspoken: gold ownership is already legal and accessible.

Georgians can purchase bullion from dealers. They can buy gold exchange-traded funds through brokerage accounts. They can store gold in private vaults. Some fintech platforms already offer gold-backed payment products.

SB 424 does not unlock access to a prohibited asset. It formalizes and lightly subsidizes an activity that already exists.

The principal tangible change would be the removal of state-level capital gains taxation on gold transactions. Federal capital gains taxes would still apply. The broader dollar-based financial system would remain intact.

This is not a monetary revolution. It is a modest regulatory adjustment framed in sweeping rhetoric.

It Does Nothing for Affordability

The article introducing SB 424 situates it in the broader debate over rising costs. That framing invites a simple question: what does this bill actually change for families struggling with everyday expenses?

Housing affordability is driven by supply constraints, zoning policy, construction costs, and interest rates. Insurance premiums are shaped by actuarial risk, litigation environments, and reinsurance markets. Healthcare costs reflect provider consolidation, opaque pricing, and payment system distortions. Wage growth depends on productivity and labor market dynamics.

A gold-backed transaction account does not increase housing supply. It does not reduce risk exposure in insurance markets. It does not lower hospital prices. It does not alter interest rates.

Even as an inflation hedge, gold is limited. While it may preserve purchasing power over long periods, it is volatile in the short and medium term and produces no income. Moreover, economic history suggests that when two monies circulate concurrently, individuals tend to hoard the one expected to retain value and spend the one expected to depreciate. If gold is perceived as “good money,” it is more likely to be saved than used for groceries.

The everyday economic pressures facing Georgians are structural. SB 424 is not.

Political Appeal Without Structural Reform

The bill’s bipartisan sponsorship gives it a veneer of consensus. It also gives lawmakers an opportunity to signal responsiveness to inflation anxiety without confronting more politically difficult reforms.

Reforming zoning laws to expand housing supply requires challenging local opposition. Stabilizing insurance markets requires grappling with litigation and regulatory complexity. Improving healthcare affordability requires confronting powerful provider systems. Those are heavy lifts.

Authorizing a gold-backed payment framework is not.

SB 424 offers the aesthetics of bold monetary reform without altering the mechanics that shape Georgia’s cost of living. It is a symbolic gesture wrapped in the language of economic freedom.

A Matter of Priorities

If SB 424 passes, the most likely outcome is modest adoption among a niche population already inclined toward precious metals. The dollar will remain dominant. Federal tax obligations will remain dollar-based. Prices, wages, and contracts will remain denominated in dollars. Inflation dynamics will continue to be shaped by national policy and global markets.

Georgia will not be insulated from federal monetary policy. It will not have solved affordability. It will have created an optional financial channel and reduced state-level tax friction on gold transactions.

That is not catastrophic. It is simply marginal.

In a time when families face real and immediate economic pressures, marginal gestures should not be mistaken for meaningful reform.

Georgia does not need goldbuggery dressed up as economic salvation. It needs serious, structural work on housing, insurance, healthcare, and productivity — the unglamorous policies that actually shape everyday life.

The shine of bullion should not distract from the substance of governance.

Charles H. Rollins, Publisher – Garden City Gossip

To See the Actual Bills:

SB 424 Legislative Tracking Link – USEFUL

And for some background on how money works:

https://www.federalreserveeducation.org/teaching-resources/economics/money/money-infographic

https://www.federalreserve.gov/aboutthefed/the-fed-explained.htm

More Editorials and Politics from GCG:

Garden City Gossip Files Open Records Lawsuit Seeking HCD Audit Records From Augusta

Augusta’s Charter Rewrite Rearranges the Furniture — But Does It Change the House?

The Quiet Rewrite of Power: Inside Augusta’s Charter Review as a Mayoral Election Approaches