Aiman Tariq – Regional News Editor

Columbia, SC –

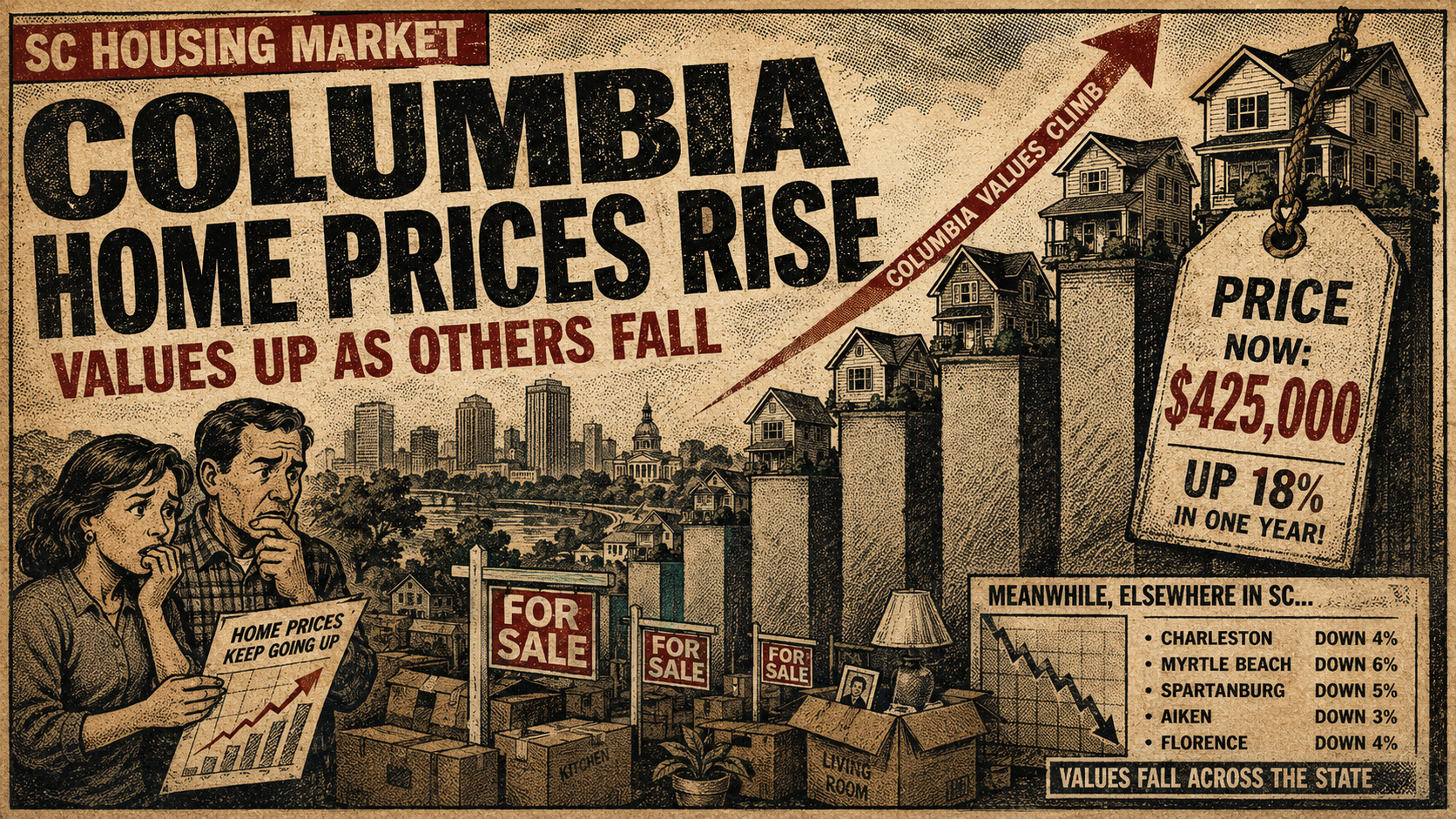

Columbia’s housing market is still moving upward, even as many large U.S. cities are seeing home values flatten or fall.

According to a new SmartAsset analysis reported by The State, Columbia ranked 20th among 100 large U.S. cities for one-year home-value growth, with the typical home value rising from $224,143 in 2025 to $226,769 in 2026. That works out to a 1.17% increase.

That is not a dramatic jump on its own. But it stands out because SmartAsset found that typical values declined in most of the cities it reviewed, with the average major-city home value falling 1.04% between 2025 and 2026.

The simplest version of the story is that Columbia prices are still rising.

The more useful version is that Columbia is moving against a softer national market — and that says something about demand, affordability, and population pressure in South Carolina’s capital.

Why Does Columbia’s Increase Stands Out?

A 1.17% increase is not the kind of number that suggests a runaway market.

It is the kind of number that becomes more meaningful when other markets are slipping.

SmartAsset’s study, which used Zillow Home Value Index data, found that 70% of the 100 major cities reviewed saw typical home values fall over the same period. Columbia’s increase placed it just behind Richmond, Virginia, and ahead of El Paso, Texas, in the ranking.

That means Columbia is not leading the country in price growth. It is not another San Francisco or New York story.

But it is holding up better than much of the market.

Zillow’s own Columbia market page shows a similar directional picture, listing the average Columbia home value at $229,068, up 1.3% over the past year, with homes going pending in about 24 days.

Those numbers do not tell the whole story. They do show that buyer demand has not disappeared.

The Longer Trend Is Bigger Than One Year

The one-year increase is modest. The longer trend is not.

According to the SmartAsset data cited by The State, Columbia home values have increased 65.2% since 2019 and 42.3% over five years.

That is the part that matters for buyers.

A one-year rise of a little more than 1% may not sound alarming. But when it comes after years of growth, even a smaller increase can keep pressure on households already struggling with higher mortgage rates, insurance costs, and limited inventory.

This is why housing numbers can be technically accurate and still incomplete.

The price is only one piece. The monthly payment is what buyers actually feel.

South Carolina’s Growth Adds Pressure

Columbia’s housing market is also being shaped by a larger state trend.

South Carolina has continued to add population, even as national population growth slowed. The U.S. Census Bureau reported that the South grew 0.9% between July 2024 and July 2025, while state-level summaries show South Carolina added nearly 80,000 people during that period.

That growth does not land evenly across every city or neighborhood.

But when a state keeps adding residents, pressure tends to show up in housing markets, especially in places with universities, hospitals, government jobs, military-adjacent employment, and regional service economies.

Columbia has several of those demand drivers.

It is the state capital. It is home to the University of South Carolina. It has major healthcare systems, public-sector employment, and a central location that makes it more affordable than some faster-growing coastal markets.

That does not guarantee prices will keep rising. It does help explain why Columbia is not cooling as sharply as many other cities.

Affordability Is Still the Catch

The same numbers can look different depending on who is reading them.

For homeowners, a rising home value can feel like stability or wealth-building. For renters trying to buy, it can feel like the door is moving farther away.

A typical value of roughly $226,000 to $229,000 still leaves Columbia far below many large U.S. markets. That is part of its appeal. But affordability is not measured only against California or New York. It is measured against local wages, household debt, mortgage rates, and down-payment savings.

That is why a market can remain “affordable” compared with other cities while still becoming harder for local residents to enter.

It is also why a modest annual increase can matter.

If prices are rising while borrowing costs remain elevated, the buyer’s actual monthly burden may grow faster than the headline home-value number suggests.

What the National Market Shows?

Columbia’s movement also stands out because several once-hot markets are moving the other direction.

SmartAsset found some of the biggest one-year declines in places such as Oakland, California; St. Petersburg, Florida; Naples, Florida; Austin, Texas; and Plano, Texas. Oakland saw a 9.07% decline, while St. Petersburg fell 7.47% and Naples dropped 6.35%, according to the study.

Those drops do not mean those markets are suddenly cheap.

They suggest that some cities that saw rapid price growth during earlier housing cycles are now adjusting.

Columbia’s market appears to be behaving differently. It is not booming at the top of the list, but it is also not giving back value in the way some large markets are.

That kind of middle-ground strength can be easy to overlook.

What the Data Can and Cannot Tell You?

Home-value data is useful, but it is not a perfect measure of what buyers face on the ground.

The Zillow Home Value Index is designed to track typical home values across markets using property-level estimates and market data. It is a broad signal, not a price tag for every street or neighborhood.

That distinction matters in Columbia.

A citywide number can smooth over major differences between neighborhoods. Some areas may see stronger price growth because of schools, commute patterns, new development, or investor activity. Other areas may be flatter, especially if homes need repairs or buyers have more choices.

There is also a difference between home values and closed sales.

A typical value tells readers where the market is estimated to be. It does not answer every question buyers care about:

- How many homes are actually for sale?

- Are sellers cutting prices?

- Are first-time buyers being outbid?

- Are investors active in certain neighborhoods?

- Are homes affordable to local workers?

Those questions require deeper local reporting.

The SmartAsset ranking is a useful starting point. It is not the whole housing story.

Why Does Columbia Keep Drawing Interest?

Columbia has a mix of factors that can support demand even in a softer national market.

It remains more affordable than many coastal cities. It has a large student and public-sector presence. It sits near major highways. It offers access to jobs, healthcare, and state government without the same price levels seen in Charleston or some fast-growing Sun Belt metros.

That combination can attract buyers who are priced out elsewhere.

It can also create tension for longtime residents.

When a city becomes more attractive to new buyers, demand can rise faster than local incomes. That is when “growth” becomes more complicated. Higher values may help current homeowners, but they can make the market harder for younger buyers, lower-income families, and renters hoping to purchase.

That is the tradeoff beneath the headline.

The Bottom Line

Columbia’s home values are still rising while much of the major-city housing market is cooling.

According to SmartAsset’s analysis, the city ranked 20th nationally for one-year home-value growth, with typical values rising 1.17% from 2025 to 2026. Zillow’s own market data shows a similar direction, with Columbia’s average home value up 1.3% over the past year.

That does not mean Columbia is in a runaway housing boom.

It does mean the city is holding up better than many large markets at a time when most of the cities reviewed in the SmartAsset study saw values decline.

For homeowners, that may look like resilience.

For buyers, it may feel like another reminder that Columbia’s affordability advantage is not guaranteed.

The real test is not whether home values rise another percentage point. It is whether the city can keep housing within reach as South Carolina grows, demand shifts, and more buyers look inland for places that still seem affordable compared with the rest of the country.